Issue 43: Want to Pay Less Taxes?

October 2023

We don't need a study to confirm that almost everyone would prefer to pay fewer taxes. Now, there is a solution that allows individuals to construct the same type of portfolio that was previously only available to incredibly large investors: Direct-Indexing (also known as Personalized-Indexing). Keep reading to discover what direct-indexing entails, how it functions, and why you can benefit from it.

TLDR Direct-Indexing involves buying individual stocks that make up an index. You buy and sell positions to generate losses while still being invested in the index. Those losses offset gains/taxes you have elsewhere allowing you to reduce taxes. I know this might sound financially wonky, I would be happy to explain it to anyone interested. It is a no-brainer for a lot of financial situations!

What is Direct-Indexing?

Before 2019, custodians such as Charles Schwab charged commissions for each trade you made. At $4.95 per trade, if you wanted to buy the S&P 500 it would cost you $2,475 (500 x $4.95). Enter Mutual Funds and ETFs, which own the underlying companies of the S&P 500 in one easy to buy fund or ETF, such as SPY.

Eliminating trading fees means there is no monetary barrier to building your own Index. You simply need to know the underlying positions, the weights they represent in the index, and monitor for changes. Enter Direct-Indexing.

How does Direct-Indexing work?

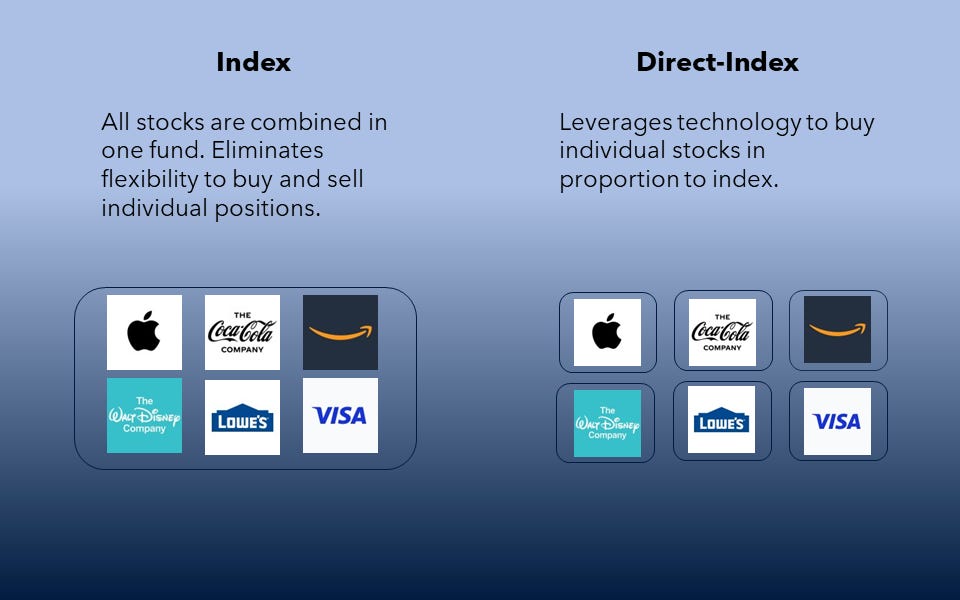

As the picture above demonstrates, Direct-Indexing breaks down an index into its constituent parts. From this simple premise, the strategy can go in a lot of different directions. Hence, why people also refer to it as personalized-indexing.

At a high level Direct-Indexing is an account designed to track an index via the purchase of the underlying stocks. Apple represents 7.15% of the S&P 500, you buy 7.15% of Apple in the account. However, you don’t really need to buy all 500 stocks to achieve diversification and high levels of correlation to the index.

What this means is you can buy 100 or 200 stocks and achieve diversification, correlation, AND FLEXIBILITY. Flexibility is key. You don’t need to own Lowe’s AND Home Depot to gain exposure to Home Improvement Retail. Just buy one. Leveraging technology, time, and attention you do this analysis across the entire S&P 500 to build a portfolio of names that correlates highly with the market while affording you the flexibility to harvest losses.

How to Harvest Losses?

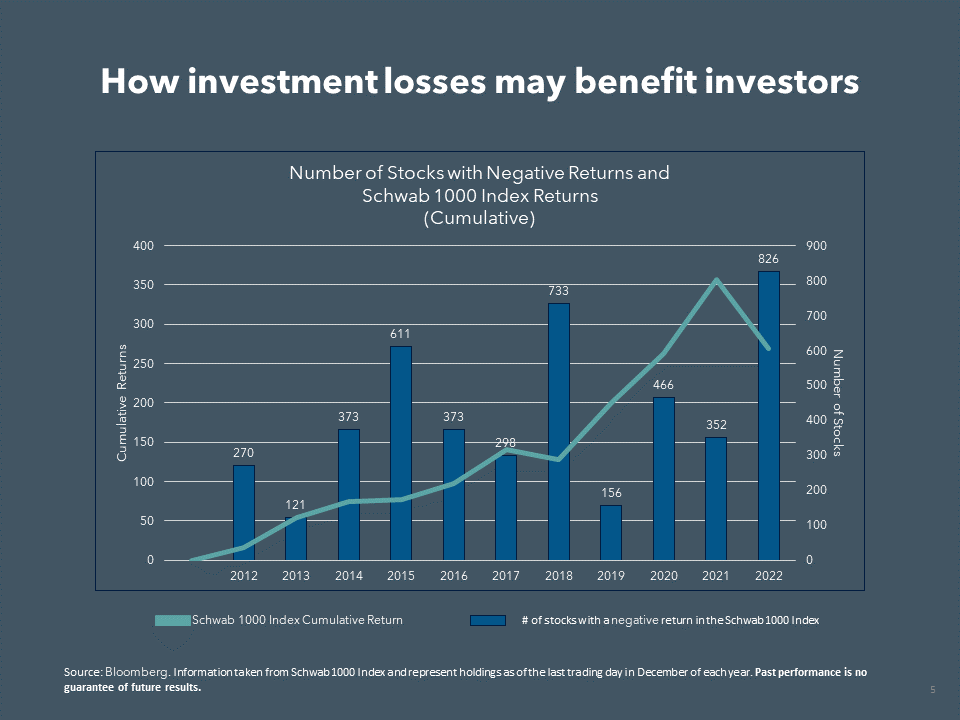

Every year there will be losers in the index. For example in 2021, the Schwab 1000 (a proxy for the S&P 500) returns 26.08%. Despite the strong return for the index, 352 stocks (35%) had negative returns.

Direct-indexing capitalizes on this dynamic. Selling losers for a tax loss while letting winners run allowing your returns to correlate to the market while taking advantage of underlying position volatility.

Why Direct-Indexing?

Reduce Taxes

Offset gains in other investments.

Mitigate taxes paid when liquidating compensation tied to company stock (RSUs, Options, etc.)

Limit taxes from selling a business, shares of a private company (via an Employee Stock Purchase Plan), real estate investment, etc.

Holistic Portfolio Construction

Customize the index to fit your situation and goals. Work in healthcare? Customize your index to reduce exposure.

Values-Based Investing

Customize the index based on your individual beliefs. Take control of ESG, religious, or political views via your index.

I am really excited about this solution as it solves a problem I know many of you encounter. If you found the article interesting, but are still unclear on how exactly it works. PLEASE REACH OUT! Implementing this strategy can build a diversified portfolio and reduce your taxes. A true win-win!

Bill