Issue 18

August 2020

Before I jump into the newsletter I want everyone to be on the lookout for an email from SCP later this month with a major announcement! With that out of the way, on to the newsletter.

I’ve spent the past few months writing about the broader market and my observations. In this issue I want to discuss an investment I made in June, the process behind it, the current situation, and implications with the broader market. The stock is Marathon Petroleum ($MPC).

From my journal on 6/10/20 -

____________________________________________________________________________

Marathon has declined ~30% YTD. As currently constructed the business is a conglomerate with ownership of three distinct parts of the energy value chain (Convenience Stores, Refining, and Midstream). The majority ownership (66%) of $MPLX (Midstream assets) by $MPC obfuscates the underlying financial statements causing the stock to screen very poorly. Importantly the activist hedge fund, Elliot has a position in the company. Through Elliot's involvement, $MPC announced they would spin off the Convenience Stores (Speedway) by the end of 2020. After our investment, $MPC revised the spin-off date to early 2021. On a positive note, they filed the paperwork (Form 10) with the SEC that is necessary to execute the tax-free spin. I view Speedway as the crown jewel of the entity and a business I want to get exposure to. We have a known catalyst coming within 6-9 months, a sector already pricing in severe disruption, and businesses relatively insulated from the wild swings of energy prices. Using an estimated value for the Retail segment, the current price for $MPLX shares, I am able to create an implied value for the Refining segment. At current prices, the Refining segment equity is worth negative $4-5b.

____________________________________________________________________________

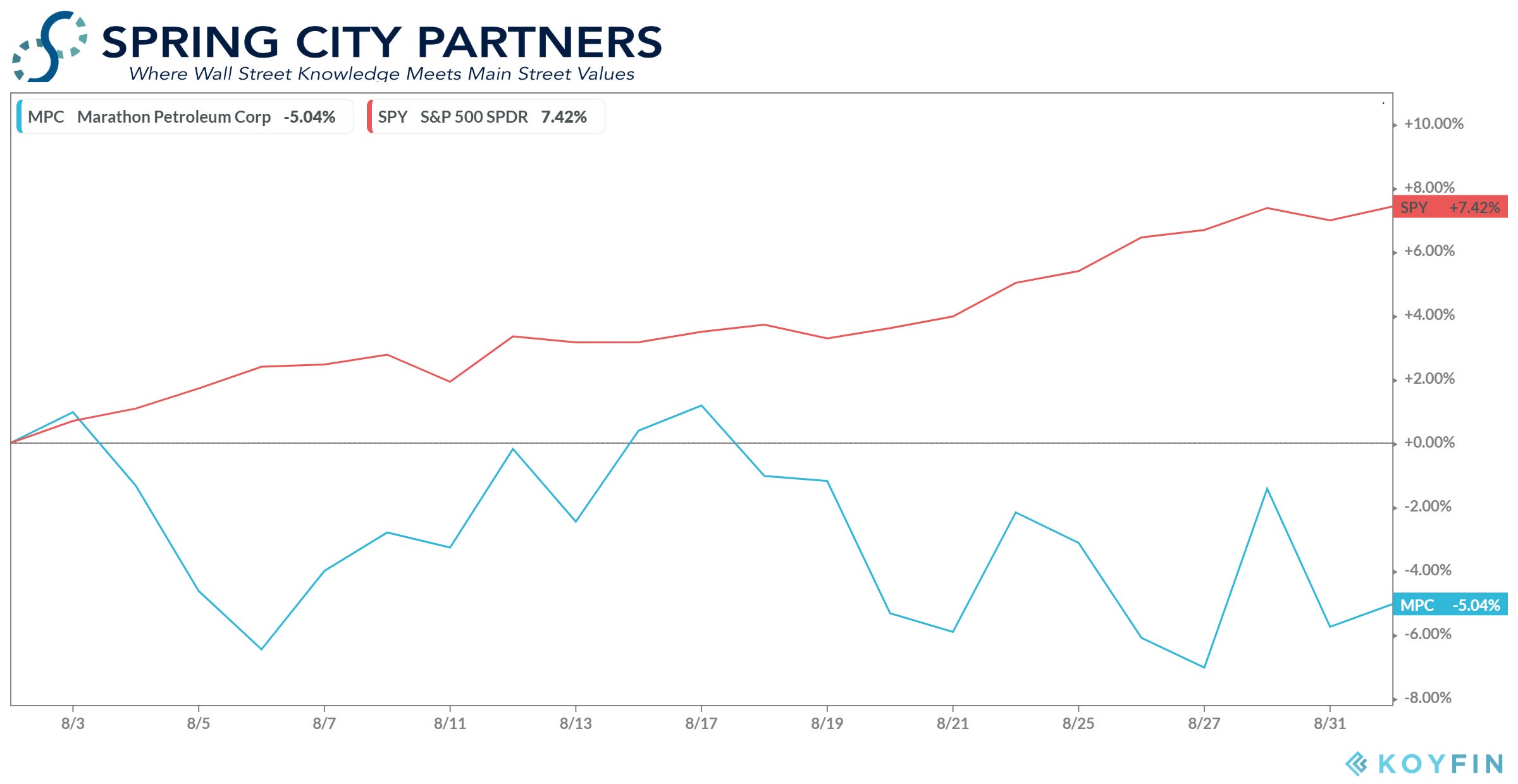

Fast-forward two months and Marathon announced the sale of Speedway to 7-11 for $21.0b ($16.5b after-tax) on 8/3/20. I valued Speedway between $16-20b. I didn’t expect taxes to eat up so much of the purchase price (22%), but my valuation work on Speedway was in the ballpark. At this point you are probably thinking, jeez Bill that was really smart. Not so fast my friend. Since announcing the deal, $MPC has declined by 5% and under-performed the S&P 500 by 12%.

Have I mentioned investing is really hard?!

If you remember my June and July newsletters, highlighted the importance of extending your investing horizons during periods of volatility and the Tech sector influence on market returns over the past couple years. In my opinion, $MPC serves as an interesting real time case study of both these threads.

Let me talk about why.

First on extending your horizons. I invested in $MPC believing they would spin-off Speedway at the end of 2020. At that point I would own the largest independent chain of Convenience Stores in the USA. There are a number of reasons why I think Convenience Stores will make a great investment over the next 5-7 years, but I’ll reserve that research for my partners. Instead $MPC sold the business and will add $16.5b in cash to the Balance Sheet. So the event I wanted to happen took place, the valuation was in-line/better than I expected, and the stock is down on the news. Maybe my analysis was wrong? (Jill, if you made it this far, take a screenshot. I don’t say those words too often.) If that is the case, then I should sell the stock. However, I think it is too early to tell. At this point this is what an investment in $MPC looks like if the deal closes by 12/31/20.

Ill elaborate on some financial metrics for the Refining segment, which encompasses most of the remaining company. A reason why I think it might be too early to tell is the Refining segment has been most impacted by the volatility in the energy markets. Time will tell if the industry normalizes or is permanently impaired by lower demand for their products.

Now, let’s talk about broader market themes. There are some noticeable signs of irrational exuberance in the market. Such as the increased trading volume from retail accounts. Or Tesla up >450% this year and 15% the day after completing a stock split. $MPC is trading at a very very cheap multiple relative to peers and the broader market, which is part of the reason I have decided to keep the position. Maybe the multiple is warranted? Time will tell.

Having an investment in a style (value) and sector (energy) that is out of vogue won’t win any beauty contests in 2020. However, investments can be like fanny packs. What was once out of style is now en vogue. Over the next five years, an investment in SCP with a portfolio of concentrated positions and minimal correlation to the market could provide a source of diversification. Dare I say, it might even be trendy to have an active portfolio alongside a passive portfolio.

If you are interested in learning more about SCP and my investment strategy, please reach out.

Bill