Passive investing is growing in popularity as a way to get cheap exposure to the broader market. I completely understand the appeal. That is one of the driving factors behind me launching the Keystone Fund last fall. However, I am a firm believer that any portfolio should have some exposure to an active strategy.

In the last issue I provided a case study of an ongoing investment, highlighting the potential risks and rewards associated with a concentrated investment portfolio. I want to expand upon the topic by explaining why concentration makes sense in the context of active investing. ——————————————————————————————————————

JP Morgan recently released an update to their study The Agony and the Ecstasy: The risks and rewards of a concentrated stock position. The report provides some good data points highlighting risks and rewards with the strategy. The chart below shows the returns of individual stocks compared to the Russell 3000. What jumps out to me is how much fatter the left tail is compared to the right. In fact, the median stock underperforms the Russell 3000.

How can the median underperform? There are two factors driving this dynamic. First, as I mentioned above the left tail has a larger number of stocks than the right side. Statistically speaking, a random stock has a higher probability of underperforming v. outperforming. Offsetting this factor is the cluster of stocks at the far right that have outperformed the Russell 3000 by >70% per year.

This encapsulates the challenge of active investing. There is a high probability a stock picked at random will underperform the market. However, if you are skillful or lucky enough to invest in stocks at the far right tail, you can generate truly mind boggling returns. And we as a society spend billions of dollars in an effort to discern which stocks will outperform the market. So how do I go about building a portfolio and selecting securities that will outperform the market?

In my opinion the two most important factors are concentration and longevity.

Concentration gets to the heart of my portfolio construction. In order to generate returns different than the market, you need to have different investments. Sounds obvious. However, take a look at two of the largest “active” investment funds Fidelity ContraFund and Growth Fund of America. Each of these “active” funds have >300 investment. In reality these funds are mirroring the return of either the S&P 500 or Nasdaq. So instead of paying <.05% for an ETF tracking the index, you are paying 0.86% and 0.64%, respectively, for highly correlated returns.

At SCP, I run a very concentrated portfolio with only 7-15 investments. As of today, I have 12 investments. The logic being I want to focus my time and investments on the right tail of that initial chart. Finding those investments and developing the conviction to own them for the long-term is very difficult.

Longevity is a critical component to both which stocks I choose to own and how I think about portfolio construction. When it comes to which stocks to own, I am constantly referencing back to this quote by Jeff Bezos,

“I almost never get the question: 'What's not going to change in the next 10 years?' And I submit to you that that second question is actually the more important of the two -- because you can build a business strategy around the things that are stable in time.”

When it comes to investments, I am looking for businesses solving a problem for customers that is going to exist well into the future. This can have many permutations. For example, they may be providing their customer with convenience, manufacturing a key component for a product, or offering a service to make their business run better. However, at its root the question is trying to understand why a business exists, how the business can evolve, and why they will exist in the future.

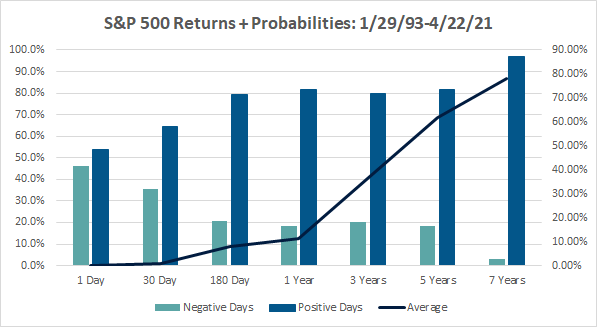

The other side of the coin for longevity at SCP, is the goal to own investments for a long period of time. I define that as 5-7 years. This isn’t something I pulled out of thin air. Instead, it is based on data around returns and probabilities for the S&P 500.

The chart above illustrates the number of Negative days, Positive days, and average period return for the S&P 500 going back to 1993. On any given day it is pretty close to a coin flip if the market will go up or down. If you extend the timeframe to one to five years, the probabilities improve dramatically with an ~80% likelihood of generating a positive return. Extend it even further to seven years and the odds become near certain with >97% likelihood of generating a positive return.

The value of focusing on these concepts was highlighted in my previous issue, where I discussed my portfolio management of Viad. I believe a concentrated portfolio allows me to better understand if new data is signal or noise. This confidence allows me to maintain conviction in the face of negative short-term information. Assuming the information doesn’t materially impact the long-term outlook of a company, I can use those opportunities to increase the size of a position. This can be painful in the short-term, but as I saw with Viad can pay enormous dividends if willing to extend your timeframe.

Have you had some recent success in the market, but realize you don’t have a real plan or strategy in place about reaching your long-term goals? I’d love to talk to you and learn more.

Bill